US Tax Residency and Foreign NPOs

Blog post description.US Tax Residency and Foreign NPOs: Disclosure Obligations

US Tax Residency and Foreign NPOs: Disclosure Obligations

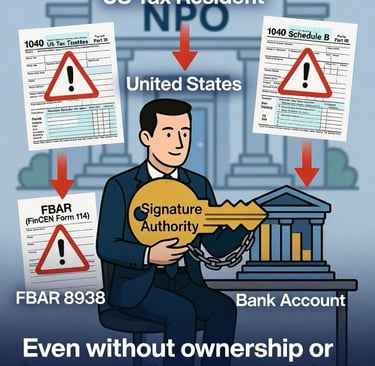

Even without ownership or personal income, managing a foreign Non-Profit Organization (NPO) triggers strict IRS and FinCEN reporting requirements for US tax residents.

Key Filing Requirements

• Form 1040 (Schedule B): Used to report worldwide income and confirm the existence of foreign accounts. It serves as a critical cross-check for the IRS.

• FBAR (FinCEN Form 114): Mandatory if you have signature authority over NPO accounts and the aggregate balance of all foreign accounts exceeded $10,000 at any time. Ownership is irrelevant; control is the trigger.

• Form 8938 (FATCA): Required if foreign financial assets exceed specific thresholds based on your filing status.

• Forms 3520 / 5471: May apply if the NPO has trust-like characteristics, receives specific grants, or involves corporate control.

Core Principle

The IRS does not automatically grant "tax-exempt" status to foreign entities. Disclosure depends on actual control, access to funds, and signature authority.

Missed Filings?

If you recently discovered these obligations, the Streamlined Filing Compliance Procedures allow for "voluntary correction." For non-willful violations, this program helps you catch up on filings while significantly reducing or eliminating penalties—provided the IRS hasn't initiated an audit yet.